At Airtree, we don't try to predict how markets will evolve. We leave that to the entrepreneurs at the forefront of their industries. But when we see a material shift in the types of businesses coming through the door, we take notice.

Over the last 12 months, that shift has been dramatic. Many founders we're meeting aren't planning to sell software into professional services firms. They want to rebuild those firms from the ground up, with technology and AI at the core.

It's a fundamentally different approach, and we think it points to where real value will be created in the AI era.

The productivity crisis

The Australian services sector is the dominant force in our economy, accounting for about 80% of national production and employing roughly 90% of the workforce. It's also facing a productivity crisis, with output lingering at pre-Covid levels.

The services sector is broad, encompassing everything outside manufacturing, agriculture and mining. But the impact AI could have on select industries within it, particularly IT, legal and accounting, is well-documented.

Done right, the rebuild model lets you deliver a better, faster, cheaper service while accruing proprietary workflow data. Margins expand as automation deepens, and you keep compounding without scaling headcount linearly.

Enterprises spent the last decade trying to automate routine work with process automation tools like UiPath. It never really worked because the tools were brittle — if a website's user interface changed slightly, the entire workflow broke.

Large language models (LLMs) are different. They enable semantic understanding, meaning models can interpret a request and deliver the right response or trigger the right workflow, even with ambiguity baked in.

Yes, LLMs are still nondeterministic, meaning you won't always get the same answer for a given query. But current advances in evals (checking answer accuracy), tool use (LLMs connecting to existing systems), and reinforcement learning (learning from expert feedback) suggest models will soon reliably deliver correct answers to users.

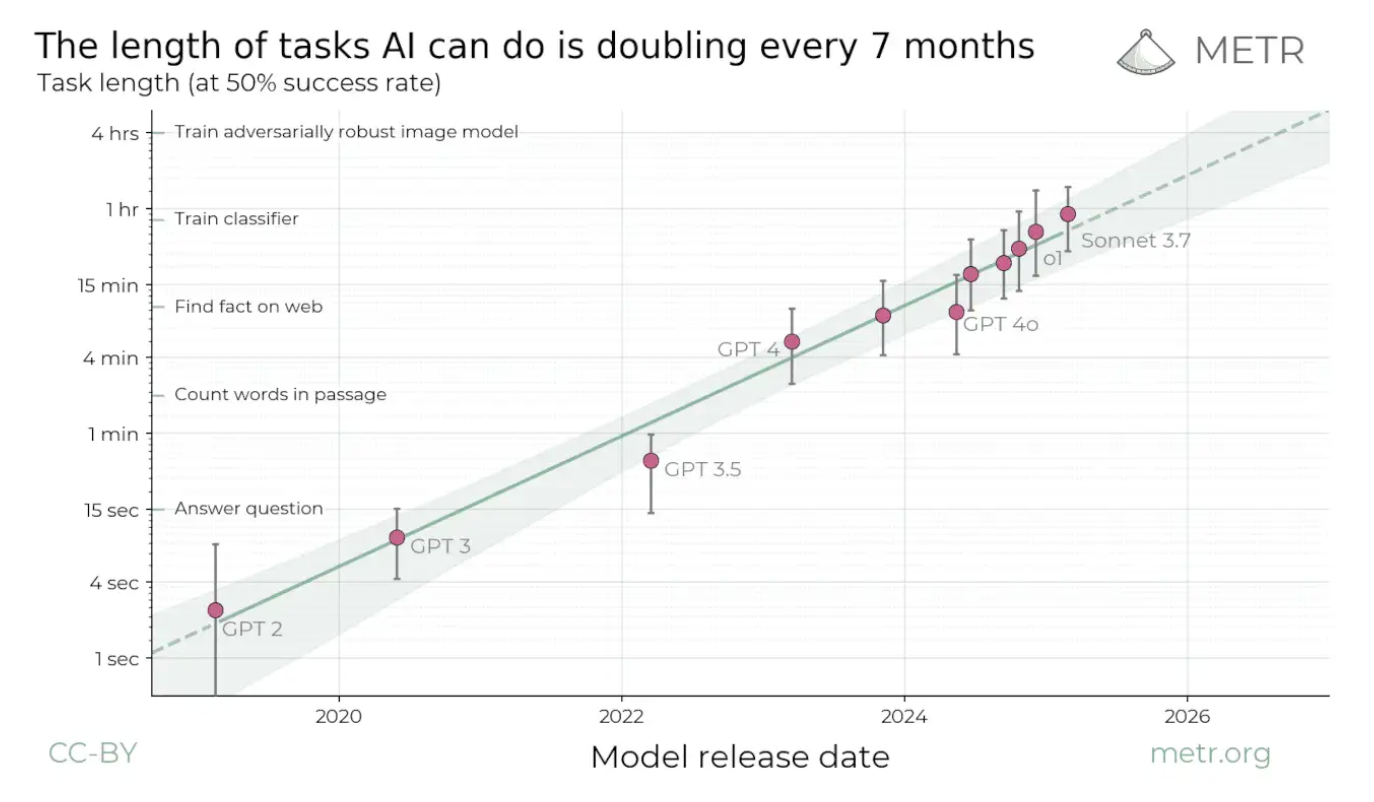

If you believe the current trend illustrated by the METR curve below continues, the complexity of workflows that AI can handle will meaningfully change in the next two years:

The enterprise versus SME divide

Most enterprises start AI implementation with customer support, where processes are clearly mapped, knowledge bases are deep, and ROI metrics are obvious.

To automate other functions, they need detailed process maps and comprehensive documentation that LLMs can use as context. Enterprise AI-native software is emerging across every function and vertical to accelerate this. We're excited about the opportunity here.

But here's the catch: while large companies can afford these tools — the productivity improvement across teams of tens or hundreds delivers meaningful ROI — SMEs often have just one or two people in a role. The dollar impact may not cover the cost of process mapping, documentation and training.

These businesses run on tight budgets. Owners don't have the time, cash flow or internal capability to fundamentally re-architect their core service delivery around new technology. To gain maximum benefit across the whole business requires invasive, complex transformation that carries significant execution risk for someone focused on day-to-day operations. It demands dedicated capital, technological expertise and strategic focus often beyond the scope of a typical SME.

Instead, over the next 3-5 years, the opportunity to capture value lies in building your own firm from the ground up as an AI-native company—and capturing the total client services revenue, not just the software revenue.

The path to venture-scale returns

Enterprise software is a highly successful business model. These businesses grow at 20-30% annually with EBIT margins of 30% or higher, for years.

This happens because of barriers to entry and exit, zero replication cost, recurring revenue that expands over time, and operating leverage as revenue scales without R&D costs scaling linearly.

A services company can earn similar economics if it dramatically improves the customer experience, automates the delivery through technology investment so revenue grows without proportional headcount growth, and builds defensibility through integrated workflows and data moats that make switching painful and copycats hard.

There will be sectors where new firms, built from scratch with technology at the core, scale through organic growth driven by sales and marketing. This works best where customers will try new providers if they deliver better experience or lower cost — marketing agencies, for example.

Whether they deliver venture-scale outcomes depends on the complexity of products and workflows they build, and the durability of that revenue. If competitors can adopt third-party AI tools to offer similar services, competition develops quickly and pricing power erodes. To invest here, we need to believe the software product can meaningfully differentiate the customer experience over decades.

Then there are sectors where customers stick with existing vendors, and acquiring them organically as a new entrant is hard. Think businesses with high switching costs, deep operational integration, contractual and regulatory lock-in, or trust and relationship moats.

In sectors handling sensitive information or providing critical advice — like accounting or NDIS support coordination — long-standing relationships built on trust are powerful, if less quantifiable, barriers to churn.

To grow in these sectors, startups can acquire customers through inorganic growth — by buying legacy businesses and transitioning those customers to the startup’s platform.

To finance acquisitions, companies raise equity and debt. The multiples they can raise at depend on their ability to show margin expansion, a repeatable M&A playbook with strong integration capability, a large addressable market, and meaningful technology differentiation that creates defensibility.

The Kismet team, for example, had already built a SaaS startup in a highly-regulated, government-adjacent sector. They were well-prepared for building software in the NDIS space but quickly realised they could scale as a plan manager, rather than by selling SaaS to plan managers. The unique characteristics of that market allowed Kismet to quickly scale as a plan manager by reimagining the NDIS participant experience through technology, then buying sub-scale plan managers and transitioning them to Kismet's technology, enabling a fast revenue ramp.

What markets we are looking at

Australia and New Zealand are service economies where companies often run on spreadsheets, phone calls and manual workflows. That's the opportunity: large markets, critical functions, still relatively untouched by technology.

We're looking at sectors where work happens behind a computer with minimal physical labour or working capital required. Ideally transactional knowledge work that's repeatable and rules-based, particularly parsing and entering unstructured data — insurance claims, expense reports, internal policy documents.

We want firms with years of returns, claims, filings and reports that AI-native companies can use to improve model accuracy, and an opportunity to automate low-value manual tasks at scale.

We're particularly interested in tech-laggard industries that are fragmented, with sticky, repeatable customer bases built on long contracts, trust-based relationships or deep customer integration.

Countercyclical industries are attractive, as are those with motivated sellers facing regulatory change or baby boomers looking to retire. Low customer and supplier concentration matters too.

This includes: insurance claims management, debt collection, managed service providers, accounting (including vertical-specific), specialised legal services, property management, managed payroll, design engineering, regulatory approvals and compliance, and wealth management.

The people behind these companies will need to look different to traditional services or software teams. Founders need deep operational experience, technology expertise, and for those scaling through acquisition, M&A capability.

These firms are something new, built for an era where the gap between technology and service delivery has evaporated. The new paradigm we inhabit is one where software and services are closely intertwined, and the positive ripple effects for businesses and their customers will be undeniable.

This piece was originally published in Capital Brief.

.png)

AirTree Ventures Custody Pty Ltd holds AFSL No. 544106.